NATO and The Military Industrial Complex

TORONTO – Last week’s NATO Conference, in Washington D.C., raised the ages-old debate of what is preferable among Allies in “world stability”: peacekeeping (negotiation capability) vs peacemaking (capacity to “shoot first and ask questions later”). Membership in the North Atlantic Treaty Organization (NATO), a post World War II alliance of mostly European nations structured to ensure peace in the face of potential enemies and invaders, seemed, generally, to work. This year, it provided a remarkable opportunity to mix local politics, economic interests, militarism and “old-fashioned jingoism”. Canada was “under the gun” – no pun intended.

Leaders who, a mere four weeks ago, had met as partners in the G-7 annual conference in Italy, seemed to go on the offensive in describing Canada as a derelict freeloader shirking responsibility towards fellow members. In other words, Canada was/is not living up to its “obligation” to ready itself for war. But “we are at peace”.

It’s complicated. Crassly put, we stand accused of not spending as much for our own defense as we have committed to do to be fully compliant with article Five of the NATO pact: spend 2% of GDP on Defense, measured in US dollars (currentl exchange rate: 1 USD = 1.36 CND). This is effectively a self-imposed minimum tax whose only beneficiary is the military industrial complex. But only 35% of the thirty-two members meet the threshold. Canada is not one of them.

For 2024-25, the federal budget’s Main Estimates forecast spending on the military at $28.8 Billion, an increase of $1.6 Billion (6%) over expenditures in 2022. According to Statistics Canada, 2024, our GDP is at c. $1.89 Trillion (Canadian). To be compliant with the principle of “spend” desired in NATO’s Art. 5, we should have allocated $37.8 Billion (to meet that 2% target in Canadian funds). The entire Budget plan envisages a $449 Billion expenditure, and a $50 Billion deficit.

It would be a challenge for any government, much less one so beleaguered as Trudeau’s, to justify an additional $9 billion, an 18% increase above the already 6% bump.

Our armed forces consist of about 66,000 active personnel; the department is serviced by a further 20,000 bureaucratic individuals and we do not have a significant weapons manufacturing infrastructure from which to purchase $9 billion of additional operational equipment (be it naval, air or land purposed).

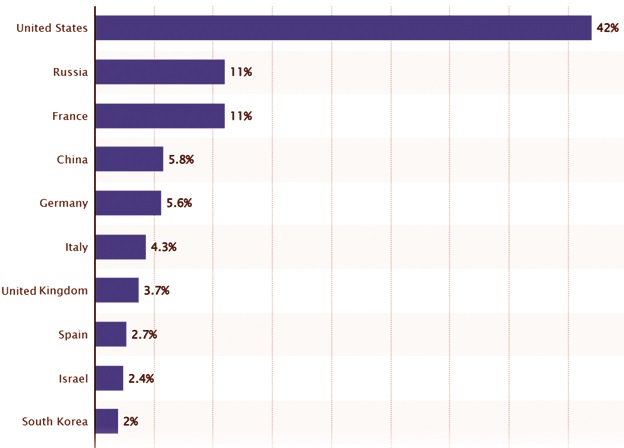

In practical terms, what would we buy; from whom? The chart below (Statista, July, 2024) provides an illuminating answer.

Sixty six percent of the export market is “owned” by our Allies – chief among them the USA – exerting pressure on us “to meet our obligations”. Statista, July 4, 2024, estimates the USA annual spend on Defense at 916 USD. At today’s exchange rate, that equals 1.245 trillion CND (two thirds the value of our GDP).

The hyper-tension by some European States in respect of the Ukraine-Russia War serves as a further incentive for action; they too are in the market for buyers. Their bravado energizes “the drums of war”, and rhetoric regarding the need to protect democracy and the principles of loyalty to common cause.

How advantageous for suppliers when “principle” demands that, even in peacetime, if a country’s GDP expands, so must its military spending – not at the rate of inflation, but at the rate of GDP growth, measured in American currency.

There is little to no money in “peace-keeping” and negotiation. In 2023, according to estimates by Statista, the weapons industrial complex generated a global value of 2.4 trillion USD, or $3.26 Trillion Canadian. It seems that “peacekmaking”, on the other hand, can be a lucrative exercise.